What will happen to my financial loss due to less or no production in the factory, due to an accident? …a very common issue which most of the corporate have to grapple with!!

A major accident in manufacturing premises not only causes damage to the physical assets, but also inflicts a severe dent in the balance sheet. The material damage policies like Standard fire and special perils policy or Machinery breakdown do not cover any loss of revenue or profit. The need for a Business Interruption policy arises because till the time the factory remains non- functional due to the operation of an insured peril like fire, flood machinery breakdown, riots etc., the corporate continues to lose revenue and also pay for the fixed costs.

What does a Business Interruption policy cover?

The Business Interruption policy covers the following, subsequent to the operation of an insured peril which should be covered under the Material damage policy e.g. (Standard fire and special perils policy, Industrial all risk policy, Machinery breakdown policy etc.):

- Loss of gross profit (i.e. Reduction in turnover / output / revenue * Rate of gross profit). This will include the standing charges or fixed costs which the corporate continue to pay when the factory is shut (i.e. rent, depreciation, salary, electricity charges, part wages, interest etc.).

- Increased cost of working: i.e. expenses incurred to expedite the process of repair or continuing the business operations by hiring an additional place/ machinery / manpower. The cost incurred should not be more than the savings made in the loss of gross profit.

Triggers for a Business Interruption claim:

The trigger for a business interruption claim arises from a condition under the policy called “Material damage provision “:

- There has to be a material damage policy like Standard fire and special perils policy or Machinery breakdown policy or IAR policy, covering the same subject matter of insurance e.g. same assets / stocks, and same location.

- The accident leading to the loss or damage must happen at the same premises which have been insured.

- The peril which has caused the loss must be covered under the material damage policy and should not be excluded under the Business Interruption policy e.g. if communicable disease is an exclusion under the material damage policy, loss due to business interruption on account of this will also not be paid.

- The claim needs to be admissible under the material damage policy for the loss to be triggered under the business interruption policy. The word “admissible “means, if Material damage loss falls within the deductible of the material damage policy, still BI loss will be payable. Let us take an example: There is a small fire (insured peril) in a factory (insured location) damaging a critical machine (insured subject matter). The material damage loss assessed is INR 450,000 towards the repair (falls within the SFSP deductible of 5 lakhs (S.I. > 100 crores). But the repair of this machine is not possible in India and has to be sent to manufacturer in Germany and time taken to get the same back is around 45 days (no replacement machine is available) …. still the BI claim for 45 days will be considered after taking into account time excess.

Can there be deviations of the Material damage condition?

Let us consider the following scenarios:

1. There is a flood in Chennai affecting many automobile parts manufacturers. Their factories have come to a standstill. One of these unit’s M/S X was the sole supplier of a vehicle manufacturer located in Gurgaon (North India) M/S Y (Our Insured). In absence of raw material M/S Y sustains Business Interruption loss. Unfortunately, triggers of a claim under a normal BI policy are not satisfied:

a) Insured location is not affected

b) Insured assets are not affected

c) No admissible loss under the insured’s material damage policy

2. Due to a riot in the city, the employees of a manufacturing unit were not able to enter the premises. In consequence, the business suffered and there was reduction in Turnover Even though insured peril operated, following parameters of trigger were not satisfied:

a) Insured location is not affected

b)Insured assets are not affected

c) No admissible loss under the insured’s material damage policy

In such scenarios, even though there are Business Interruption losses due to insured peril operating, the claims are not triggered under the BI policies ……a contingent situation, no doubt!!!

Contingent business interruption covers (which are optional extensions under a Fire loss of profit policy) like Suppliers’/ Customers premises extension (Scenario 1) and Prevention of access extension (Scenario 2), provide protection against such deviations of Material Damage provision. These add- on covers operate with a sub limit

For how long a Business Interruption claim can be paid?

The policy will be carrying an indemnity period, which is different from the policy period and represents insured’s guess of the maximum interruption which an accident can cause. This period can range between 3 months to 36 months.

The policy pays:

- As long as the actual interruption period is within the chosen indemnity period.

- If the interruption period is > Indemnity period, the claim is paid till the indemnity period.

- Interruption period starts from the date of loss and goes on till the insured do not reach the level of production just prior to the accident i.e. till it does not attain “commercial readiness “

What is the Sum Insured under the Business Interruption policy?

Annual Gross Profit “represents the sum insured under a business interruption policy. In case the Indemnity period is > 12 months, the annual gross profit should be proportionately increased.

The gross profit ideally should be calculated as follows: Annual turnover of the company Less the Variable costs

How to arrive at the right Gross profit?

Suggested Method of arriving at the GP:

- Gross profit (turnover) from last available balance sheet to be considered. If the policy is to be renewed on 1st April, 2025, the last available figures could be as on 30th September, 2024. (Step 1)

- This figure needs to be extrapolated till 31st March, 2025 and then further inflated / deflated based on expected growth/ de-growth during the FY 2025-26 (Step 2)

- The loss can happen on the last day of the policy. Hence depending on the Indemnity period chosen (12 months here) the figure arrived at step 2 needs to be further extrapolated.

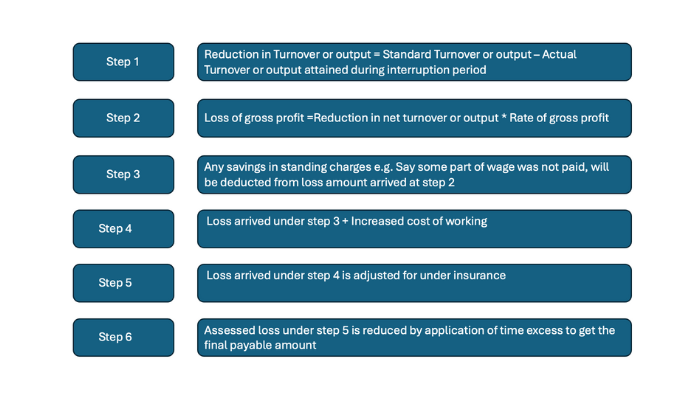

General Steps Followed for Loss Assessment

Note:

- In case some savings have been made by attaining turnover from other premises the same will be Deducted from the reduction in T.O. In the insured premises to get reduction in net T.O. (Step 1)

- Trends adjustment or Special circumstances clause can be used to adjust reduction in turnover. (Step 1)

- Under a business interruption policy, underinsurance applies if … Rate of gross profit * Annual turnover is MORE than the gross profit insured …….

For IP > 12 months, annual turnover would also be proportionately INCREASED.

- Annual TO represents the Turnover during the twelve months immediately before the date of the Loss.

- The policies carry a Time excess i.e. deductible expressed in the form of a “non-indemnifiable period “. Under normal fire policies the deductible will be 7 days of standard gross profit whereas under most Machinery breakdown Loss of profit policies, it will be 14 days of standard gross profit.

Disclaimer: The above blog is based on the current market practices. However, the respective insurers’ decision/ interpretation in this regard will be deemed to be final and legally binding. The blog is of a suggestive nature and for the guidance and academic interest only